Must Read

Jollibee’s MSCI downgrade formalizes what sophisticated investors were already starting to see below the surface: Jollibee’s financial status has moved into a tougherJollibee’s MSCI downgrade formalizes what sophisticated investors were already starting to see below the surface: Jollibee’s financial status has moved into a tougher

[Vantage Point] The uncomfortable math behind Jollibee’s MSCI demotion

이 콘텐츠에 대한 의견이나 우려 사항이 있으시면 crypto.news@mexc.com으로 연락주시기 바랍니다

Jollibee’s downgrade from the MSCI Philippines Standard Index into the small-cap tier is more a warning signal than a technical market event. It reduces the stock’s visibility among global institutional investors and triggers portfolio allocations. Beneath the iconic brand and aggressive international expansion lies a more complicated financial reality: rising debt costs, tightening liquidity, mounting lease obligations, and a business model increasingly dependent on continuous expansion to sustain growth momentum.

This forensic analysis reveals how this beloved Philippine consumer empire has evolved from a straightforward fast-food success story into a highly leveraged global roll-up now operating under far stricter financial and market scrutiny.

The relegation of Jollibee Foods Corporation from the MSCI Philippines Standard Index to small-cap is not just an embarrassing portfolio adjustment. It is a forensic event.

Markets don’t demote businesses based on nostalgia, brand affection, or national symbolism. They demote them with liquidity, valuation dynamics, balance-sheet flexibility, and institutional confidence — all slowly turning off the boil.

And underneath Jollibee’s happy face and nonstop international growth narrative, the financial statements have now exposed a company in the throes of a much more ominous stage of corporate evolution.

In order to truly appreciate why this is important, you need to get a handle on what MSCI actually is. Morgan Stanley Capital International, or MSCI, started in the late 1960s as a global stock market indexing and analytics agency as a place to help institutional investors measure and compare markets worldwide.

Over time, MSCI became one of the most powerful gatekeepers of global capital. Today, trillions of dollars that are managed by pension funds, sovereign wealth funds, insurance companies, and exchange-traded funds refer to MSCI indices to help determine how money should flow.

In plain English, MSCI serves as a global scorecard for publicly listed companies. Giant international investment funds often buy or hold the equity of a company that gets listed in the main MCSI index.

There are a two main country indices in the MSCI. There’s an MSCI Philippines Standard Index and an MSCI Philippines Universal Index. It’s important to distinguish the two because they serve different purposes in global investing.

The Standard Index is MSCI’s primary benchmark for Philippine large- and mid-cap companies — effectively the country’s institutional “main stage” followed by many global emerging-market funds, pension managers, and passive investment vehicles.

The top 10 publicly listed Philippine companies in the MSCI Philippines Standard Index (the main large/mid-cap benchmark). Screenshot from MSCI Philippines Index

The top 10 publicly listed Philippine companies in the MSCI Philippines Standard Index (the main large/mid-cap benchmark). Screenshot from MSCI Philippines Index

Inclusion signals that a stock possesses sufficient market capitalization, liquidity, and institutional relevance to warrant meaningful global investor exposure. Removal from that benchmark, therefore, is not merely cosmetic. It can trigger automatic portfolio outflows and reduce the stock’s visibility among foreign institutional investors.

The Universal Index, by contrast, is a broader strategy-based derivative index that incorporates additional portfolio and ESG-style overlays. While useful for specialized funds, it does not carry the same signaling power as the Standard Index itself.

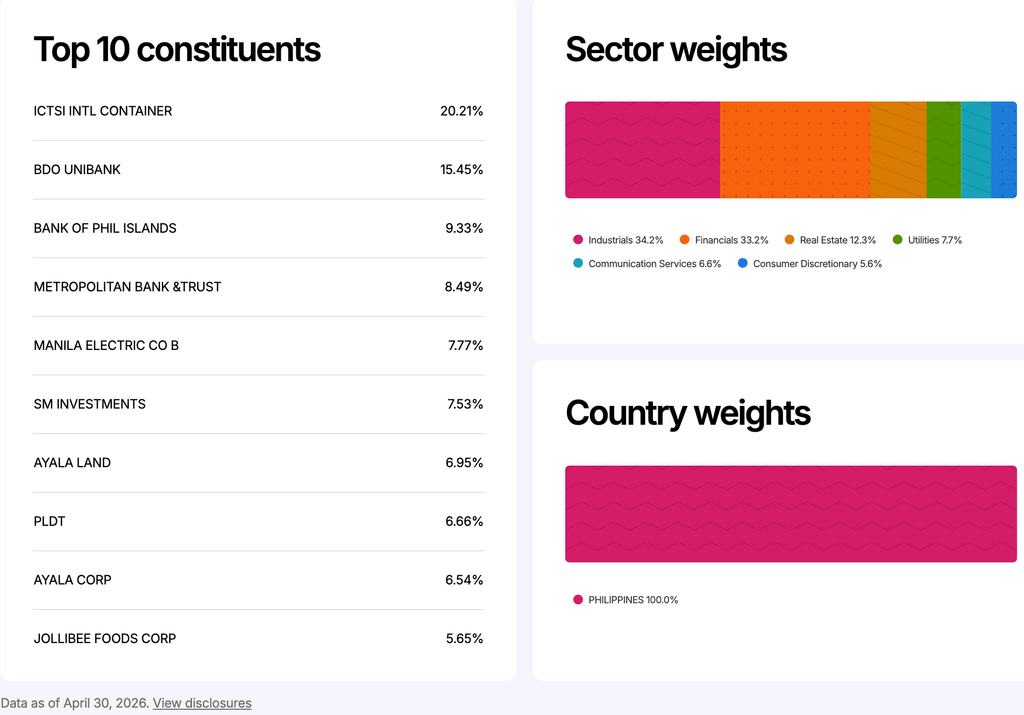

These graphs from MSCI’s Universal Philippine Index (as of April 30, 2026) shows Jollibee at only 5.65% weighting in the MSCI Philippines ETF. These demonstrate that Jollibee has become a smaller institutional weighting relative to names like ICTSI, BDO, and BPI, which indicate that global passive funds increasingly view Jollibee as less central to the Philippine institutional equity story. Screenshot from MSCI Universal Philippines Index

These graphs from MSCI’s Universal Philippine Index (as of April 30, 2026) shows Jollibee at only 5.65% weighting in the MSCI Philippines ETF. These demonstrate that Jollibee has become a smaller institutional weighting relative to names like ICTSI, BDO, and BPI, which indicate that global passive funds increasingly view Jollibee as less central to the Philippine institutional equity story. Screenshot from MSCI Universal Philippines Index

This distinction matters in Jollibee’s case because its downgrade was tied to the main MSCI Philippines Standard Index — the benchmark global investors closely watch when assessing which Philippine companies remain part of the country’s core institutional equity story.

What it means

When a company is downgraded into a smaller category, those funds automatically cut exposure or exit altogether. This is why Jollibee’s downgrade matters. While it does not mean the company is collapsing, uncertainty rises among global investors about Jollibee’s continued inclusion in the country’s premier institutional-grade stocks.

The reason is explained in the company’s financials. Jollibee is not financially distressed. It still recorded close to P305 billion in revenues for 2025, compared with about P270 billion the prior year. Net income attributable to shareholders increased a little to around P10.9 billion. Millions of Filipinos still patronize Jollibee stores, and the brand remains one of the strongest consumer franchises in the country. Deeply understanding Jollibee’s financials isn’t just about revenues, but about the quality of growth, and how much financial strain is required to sustain it.

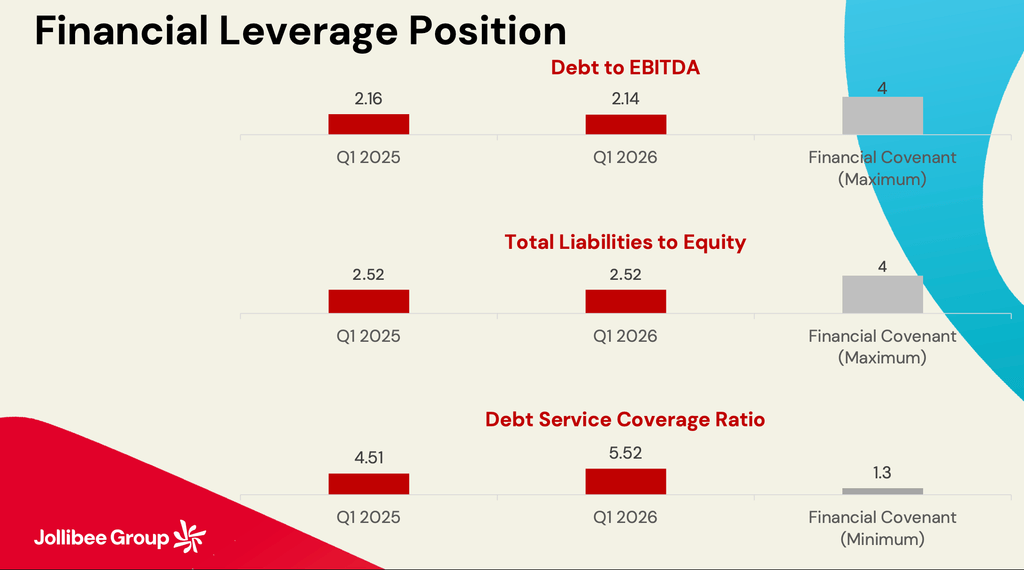

This slide on leverage ratios shows the Jollibee Group remains comfortably within its bank-covenant thresholds. Debt-to-EBITDA at around 2.14x is still below the 4.0x covenant ceiling. Debt-service coverage at 5.52x is also well above the minimum 1.3x requirement. This means lenders are not yet treating Jollibee as financially stressed. In fact, from a pure banking perspective, the company still looks serviceable and compliant. Image from Jollibee Group’s Q1 2026 Earnings Call/May 15, 2026

This slide on leverage ratios shows the Jollibee Group remains comfortably within its bank-covenant thresholds. Debt-to-EBITDA at around 2.14x is still below the 4.0x covenant ceiling. Debt-service coverage at 5.52x is also well above the minimum 1.3x requirement. This means lenders are not yet treating Jollibee as financially stressed. In fact, from a pure banking perspective, the company still looks serviceable and compliant. Image from Jollibee Group’s Q1 2026 Earnings Call/May 15, 2026

This is where the pressure becomes visible. Interest expense surged to roughly P7.6 billion from P5.8 billion in just one year, growing much faster than actual earnings. That matters because rising finance costs quietly reduce the economic efficiency of expansion. A company can continue opening stores and reporting higher revenues, even as it becomes financially tighter underneath.

Jollibee debts outstrip assets

Liquidity metrics reveal the same pattern. Current liabilities now exceed current assets, pushing Jollibee’s current ratio below 1.0. In other words, short-term obligations are now larger than readily available short-term resources. This does not mean insolvency is imminent. Jollibee still possesses strong banking relationships, enormous scale, and healthy operating cash flow. But it does mean the business increasingly depends on uninterrupted cash generation and stable refinancing condition.

The Jollibee Group is now a global enterprise that is a far cry from the traditional company many investors still picture. For decades, Jollibee was regarded as one of the cleanest tales in Philippine capitalism: a homegrown fast-food chain beating global juggernauts through a blend of cultural acumen and discipline in operations.

Today, the firm has become a multinational acquisition center dependent on its debt markets, leases, and perpetual expansion to keep rising. That distinction completely changes its financial risk profile.

Operating cash flow was robust at approximately P36.7 billion. Capital outlays, however, exceeded a P15 billion budget, while leases were eating up nearly P12 billion. Interest payments, dividends, refinancing obligations, and acquisition-related costs reduced liquidity even more. This is probably what most retail investors overlook: being profitable on paper is not the same as generating available cash.

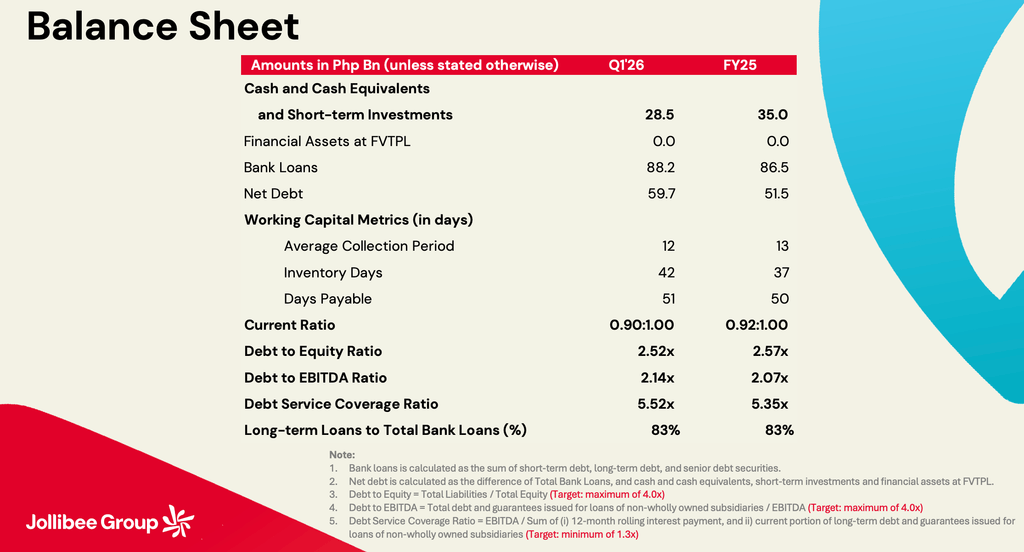

Several metrics stand out from this balance sheet: Cash and short-term investments fell from ₱35 billion to ₱28.5 billion; Net debt increased from ₱51.5 billion to ₱59.7 billion; Bank loans rose from ₱86.5 billion to ₱88.2 billion; Inventory days increased from 37 to 42 days. Current ratio weakened from 0.92x to 0.90x. None of these metrics signals crisis. But collectively, they show a company increasingly consuming liquidity while debt obligations continue climbing. Image from Jollibee Group’s Q1 2026 Earnings Call/May 15, 2026

Several metrics stand out from this balance sheet: Cash and short-term investments fell from ₱35 billion to ₱28.5 billion; Net debt increased from ₱51.5 billion to ₱59.7 billion; Bank loans rose from ₱86.5 billion to ₱88.2 billion; Inventory days increased from 37 to 42 days. Current ratio weakened from 0.92x to 0.90x. None of these metrics signals crisis. But collectively, they show a company increasingly consuming liquidity while debt obligations continue climbing. Image from Jollibee Group’s Q1 2026 Earnings Call/May 15, 2026

Too many cooks spoil the broth

A company may report billions in earnings, while simultaneously operating under growing financial pressure because too many parties are competing for the same cash flow stream. In Jollibee’s case, creditors require debt servicing, landlords demand lease payments, shareholders expect dividends, and global expansion requires fresh investment capital.

The increase of goodwill and intangible assets must also be closely considered. Years of acquisitions pushed goodwill and trademarks toward levels approaching the scale of shareholders’ equity itself.

Goodwill, of course, is really an accounting statement of optimism — the price management pays as a premium for the high expectations of the enterprise, driven by the belief that any acquired business will bring strong future profits and long-lasting value,

As long as those acquisitions keep doing well, the strategy pays off. But the larger the goodwill becomes, in relation to equity, the more vulnerable the balance sheet is, if growth slows or foreign operations fall short.

This is precisely why the MSCI downgrade should not be treated as a one-time technical fix. It formalized what sophisticated investors were already starting to see below the surface: Jollibee’s financial status has moved into a tougher period in which growth alone is no longer sufficient.

Investors want stronger free cash flow, better liquidity, and more stability in the balance sheet. Capital markets function with mathematics, not love. Investors care more about hard numbers than brand loyalty. That same math is now wondering whether Jollibee’s worldwide empire can keep growing without expanding the financial architecture that underpins it. – Rappler.com

Click here for more Vantage Point articles.

시장 기회

메스 가격(MATH)

$0.03271

$0.03271$0.03271

USD

메스 (MATH) 실시간 가격 차트

면책 조항: 본 사이트에 재게시된 글들은 공개 플랫폼에서 가져온 것으로 정보 제공 목적으로만 제공됩니다. 이는 반드시 MEXC의 견해를 반영하는 것은 아닙니다. 모든 권리는 원저자에게 있습니다. 제3자의 권리를 침해하는 콘텐츠가 있다고 판단될 경우, crypto.news@mexc.com으로 연락하여 삭제 요청을 해주시기 바랍니다. MEXC는 콘텐츠의 정확성, 완전성 또는 시의적절성에 대해 어떠한 보증도 하지 않으며, 제공된 정보에 기반하여 취해진 어떠한 조치에 대해서도 책임을 지지 않습니다. 본 콘텐츠는 금융, 법률 또는 기타 전문적인 조언을 구성하지 않으며, MEXC의 추천이나 보증으로 간주되어서는 안 됩니다.

추천 콘텐츠

Moody’s Assigns First-Ever Rating to Bitcoin-Backed Municipal Bond in Historic Crypto Finance Move

TLDR: Moody’s assigned a provisional Ba2 rating to a $100M Bitcoin-backed New Hampshire municipal bond, a market first. The bond requires 160% Bitcoin overcollateralization

공유하기

Blockonomi2026/04/02 18:15

Hyperliquid Faces Perpetual Futures Test From OKX And NYSE’s Parent Company

Hyperliquid (HYPE) has been setting the pace in the perpetual futures market but that lead is facing a new test after OKX—along with Intercontinental Exchange (

공유하기

Bitcoinist2026/05/23 13:00

How Air Freight Helps Businesses Avoid Costly Downtime When Critical Parts Are Delayed

In many industries, one delayed part can create a much bigger problem. A machine may stop running, a construction project may slow down, a retail launch may miss

공유하기

Techbullion2026/05/23 13:12

인기 뉴스

더보기