Can Decentralized Finance Truly Fix Global Credit Inequality, or Will New Forms of Exclusion Emerge?

In 2022, during Canada's Freedom Convoy protests, something happened that changed my view on financial freedom. Over 200 bank accounts were frozen without notice, leaving protesters unable to access their money. Imagine waking up to find your debit card doesn't work, not because you're out of money, but because a government official didn't like your political views.

\

\ This didn't happen in a faraway authoritarian country. It happened in Canada, known for its democratic values. Yet, with a few keystrokes, the financial system was used as a tool for control.

This event highlighted what many of us have felt for years: traditional finance isn't just slow or costly. It's a system with hidden gatekeepers who decide who can access money, credit, and economic opportunities.

\

The Invisible Hand of Financial Censorship

\ Financial censorship doesn't make big news. It works quietly, with credit scores that drop for no clear reason, loan applications that vanish, and algorithms that seem to target certain groups.

Think about this: the Consumer Financial Protection Bureau says 7 million Americans have no credit record at all. Another 13.5 million have records too thin to get a score. That's about 20 million people shut out of the financial system, not because they're irresponsible, but because they haven't had a chance to prove themselves with traditional credit scoring.

Here's the interesting part. Many of these "credit invisible" people have been paying back loans for years, just not to banks. They've been paying microfinance institutions, community lenders, and fintech platforms outside the usual credit system. Their perfect payment history is ignored.

This is where Creditcoin enters the picture, like a digital archaeologist uncovering buried financial histories.

\

The Promise of Creditcoin's Decentralization

Creditcoin operates on a simple but revolutionary premise: every loan repayment, no matter how small or from which platform, gets recorded on an immutable blockchain ledger. Think of it as a global credit history that no single institution controls.

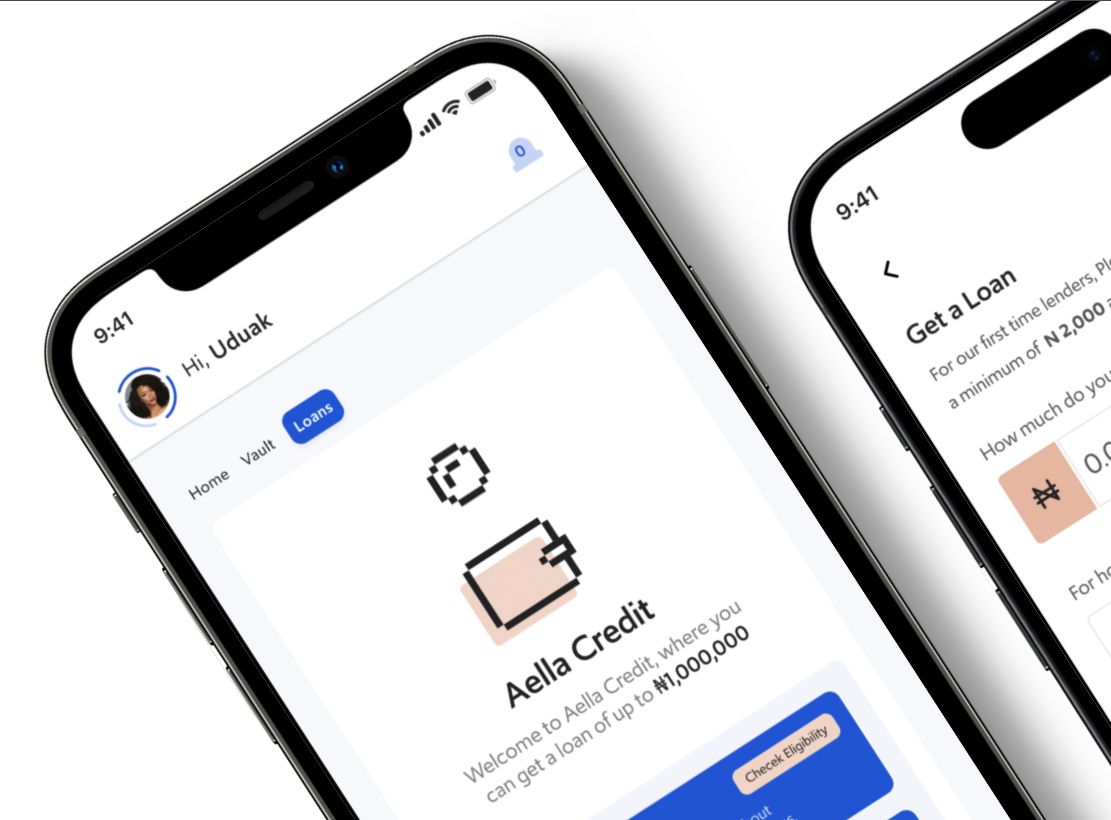

\ When a borrower in Nigeria repays a microloan through Aella, that transaction gets cryptographically logged on Creditcoin's network. When someone in Kenya makes their monthly payment to a fintech lender, it's recorded. When a small business owner in Brazil pays back a peer-to-peer loan, the blockchain remembers.

Over time, these individual transactions weave together into something unprecedented: a portable, verifiable credit history that belongs to the borrower, not to any bank or credit bureau.

The numbers are already impressive. Through partnerships with financial institutions like Aella, over 100 billion Naira has been disbursed to more than 2 million Nigerians, with every transaction building toward a decentralized credit infrastructure.

But the real magic happens when this data becomes interoperable. Imagine a world where your credit history follows you across borders, platforms, and financial systems. Where a loan you repaid in Lagos counts toward your creditworthiness in London. Where your financial reputation truly belongs to you.

\

New Gatekeepers in Digital Clothing

As I've learned from studying technology, every solution brings new problems. The question isn't if decentralized finance will remove gatekeepers, but if the new gatekeepers will be better than the old ones.

We're already seeing some worrying trends. DeFi protocols, even though they claim to be decentralized, often give power to a few big token holders. Decisions are made by those with the most tokens, not necessarily by those who are the wisest or fairest.

Look at the infrastructure layer: data oracles that provide information to smart contracts, KYC providers that check identities, and the few companies that control the connections between different blockchains. These could become new bottlenecks, possibly more powerful than traditional banks because they have less oversight.

https://youtu.be/7lHhS3KiWgE?embedable=true

There's also the validator issue. In Creditcoin's Nominated Proof-of-Stake system, validators with more tokens have more control over the network. While this encourages security, it also means that wealth gives power, a pattern we've seen before in traditional finance.

Even more subtle is the risk of algorithmic bias creeping into decentralized systems. If the data used to train credit assessment models reflects historical inequalities, blockchain immutability could actually make discrimination harder to fix, not easier.

\

The Idealism vs. Implementation Gap

Here's where the rubber meets the road: can a truly open financial system coexist with the regulatory realities of the modern world?

Financial regulations exist for legitimate reasons. Anti-money laundering laws help prevent terrorism financing. Know Your Customer requirements reduce fraud. Consumer protection rules shield people from predatory lending.

But compliance mechanisms in DeFi often look suspiciously like the centralized systems they're supposed to replace. Users suddenly find their funds frozen without explanation. Smart contracts implement blacklists that can't be appealed. The promise of "permissionless finance" collides with the reality of regulatory compliance.

The irony is stark: DeFi was created as a space free from traditional regulation, yet users now face AML mechanisms without the legal protections that exist in traditional banking.

As one researcher noted in a recent study on DeFi governance: "Users remain completely defenseless against potential abuse. This is especially ironic, as DeFi was created as a space free from regulation, yet users are now subject to Anti-Money Laundering mechanisms without legal recourse."

\

Building a Fair Credit System

\ So what would it actually take to build a fair credit system? The answer isn't purely technological, it's about the values we embed in the code.

First, we need transparent governance. Every decision about how credit is assessed, who gets access, and how disputes are resolved should be open to public scrutiny. The algorithms that determine creditworthiness should be auditable, not hidden behind proprietary black boxes.

Second, we need inclusive design from the ground up. This means actively seeking out and incorporating feedback from underserved communities, not just building for the crypto-native elite. It means designing systems that work for people with irregular incomes, limited digital literacy, and diverse cultural contexts.

\

\ Third, we need reputation systems that users can take with them. Your credit history should be yours to manage, share, and benefit from, not something a company can use against you.

Finally, we need strong ways to resolve disputes. When algorithms make mistakes, and they will, there should be easy ways to challenge decisions and fix errors.

Creditcoin is taking steps in this direction. Its blockchain-agnostic design allows for interoperability across different financial platforms. Its focus on recording real-world loan performance creates credit histories based on actual behavior, not just traditional metrics. And its partnership approach with existing fintech lenders provides a bridge between the old system and the new.

\

The Vision: Credit That Belongs to You

The main goal isn't to replace banks with blockchain but to create a financial system where your reputation is yours, not owned by a company.

Imagine a world where a small business owner in Mumbai can get loans based on her record of paying back small loans, even without a big bank connection. Where a new immigrant can build credit by showing they are financially responsible in different ways. Where your financial history is portable, verifiable, and truly yours.

This isn't just about technology; it's about fairness in the economy. When credit is truly accessible and fair, it unlocks human potential on a large scale. Entrepreneurs can start businesses. Families can buy homes. Communities can invest in their futures.

But to achieve this vision, we need to be careful. We must make sure that in fixing the problems of traditional finance, we don't create new forms of exclusion that are even harder to spot and fix.

The blockchain remembers everything, but it's up to us to ensure it remembers fairly.

As we stand at this crossroads between the old financial system and the new, the question isn't whether decentralized finance will transform credit; it's whether we'll have the wisdom to guide that transformation toward justice rather than just efficiency.

The code is being written now. The choices we make today will determine whether blockchain becomes a tool of liberation or just another form of digital control.

The future of credit is being built one transaction at a time. Let's make sure it's a future we actually want to live in.

\

You May Also Like

American Bitcoin’s $5B Nasdaq Debut Puts Trump-Backed Miner in Crypto Spotlight

‘Compromise is in the air’: Ripple CLO signals progress on crypto bill